#3 Blog

How a CO2 pipeline network in Switzerland could be governed and financed

July 2023 – by Oliver Akeret & Martynas Bagdonas, Sustainability in Business Lab at ETH Zurich

In August 2022, for the first time ever, CO2 captured from a waste-water treatment plant in Switzerland was transported to Iceland for injection and mineralization in geological formations underground in the context of the pilot project DemoUpCARMA.

The choice of Iceland as a storage site, which significantly extends the length of the transport route, is no coincidence. Research projects have shown limited potential for storing CO2 in geological storage formations in the near future in Switzerland. Therefore, exploring alternative storage options is critical. After capturing the CO2 at ARA Bern, the CO2 is liquefied and loaded onto portable ISO containers with a capacity of 20 tons, which can keep the CO2 in a liquid state until arrival at the storage site. The ISO containers are transported via truck from ARA Bern to the train station in Weil am Rhein. From there, the CO2 is transported first via rail to Rotterdam and then via ship to Reykjavik. Once delivered in Reykjavik, the ISO container is transferred to the injection site via truck.

From pilot transport to scale-up

This rather complicated travel route characterizes the pilot stage of the project. In this sense, the pilot’s main goal is to prove the general feasibility of a CO2 value chain in order to already address potential techno-economic and regulatory gaps prior to scale-up and further development of such CO2 value chains. The findings from this pilot project will prove to be eminently important when considering the quantities of CO2 that will have to be captured, transported, and stored at scale in the longer term.

The Swiss long-term climate strategy estimates 7 million tons of CO2 per year will need to be captured, transported, and stored by 2050 to achieve net-zero. Even assuming that closer storage sites would be available by then, such quantities of CO2 can no longer be transported in ISO containers and with trucks, trains, or ships. In this scenario, a larger CO2 pipeline network that collects captured CO2 in Switzerland and then transfers it to a larger trans-European will be required. To plan for this, in the context of the DemoUpCARMA project, the Sustainability in Business Lab at ETH Zurich investigated different organizational and financial aspects of such a CO2 infrastructure in Switzerland, considering potential sources of funding and revenue, and who would own the pipeline network.

What would the pipeline network look like?

In 2021, Saipem and the Swiss Association of Waste Disposal Facility Operators (VBSA) conducted a study [1] analysing the feasibility and costs of a CO2 pipeline network in Switzerland. The study allows to draw initial conclusions about what such a pipeline network covering the 7 million tons of CO2 per year outlined in Switzerland’s long-term climate strategy could look like: It would span around 1,000 kilometres (see Figure 1). This network would consist of two main pipelines (east and west) with smaller flowlines connecting directly to emitters. The pipelines would converge in Basel, which could eventually link the Swiss CO2 network to a larger trans-European network. The emitters considered in this study were those that emit at least 100,000 tons of CO2 per year, which covers 32 large emitters from hard-to-decarbonize sectors such as cement or waste-to-energy.

Figure 1: CO2 pipeline network infrastructure in Switzerland

How much would it cost and who would pay for it?

The pipeline study estimated initial investment costs of around EUR 3 billion, with yearly operational costs of approximately EUR 200 million. It is important to note that such large investments are not unprecedented in Switzerland considering the FABI expansion programme for the train network (CHF 6.4-12.9 billion) or the NEAT Gotthard-Basistunnel construction (CHF 23 billion).

Given the strong credit position of Switzerland, from a purely financial point of view, public funding would be the most cost-efficient way to finance such a CO2 pipeline network. However, the Federal Constitution currently only provides the basis for the development of energy technologies at the federal government level, and it is rather unclear whether a CO2 pipeline network could fall into this definition. Assuming that public funding would need to be regulated at the cantonal level, the key challenge becomes the coordination among them. Given the number of investment decisions that need to be taken and various interdependencies, the set-up of a centralized funding and ownership entity would probably be necessary to optimize the process and, hence, reduce the overall costs. These limitations in mind, (partial) private funding could also be considered desirable, for instance to increase the amount of available funding, share some of the risks with the private sector, or make use of operational skills available in the group of funders.

To recoup some of the initial investment costs, but especially to cover the continuing operational costs, it is important to consider possible revenue streams from the CO2 pipeline network’s operation. Several revenue models could be foreseen to establish a constant stream of payments: subsidies from the state or the cantons mainly generated through tax revenue would pass on part of the costs to society. At the same time, cost-reflective tariffs for emitters that use the CO2 pipeline network or taxes on all emitting industries that could be connected to the pipeline could be considered. Also, a hybrid setup combining both models could be foreseen. In many regulatory frameworks across Europe, the tariffs or taxes for emitting industries are applied for financing network assets. However, with the Swiss society benefitting from climate protection in general and the relevant emitters expected to benefit from the resulting CO2 savings in particular, the use of a different or hybrid model could be envisioned.

How and by whom would the pipeline be managed?

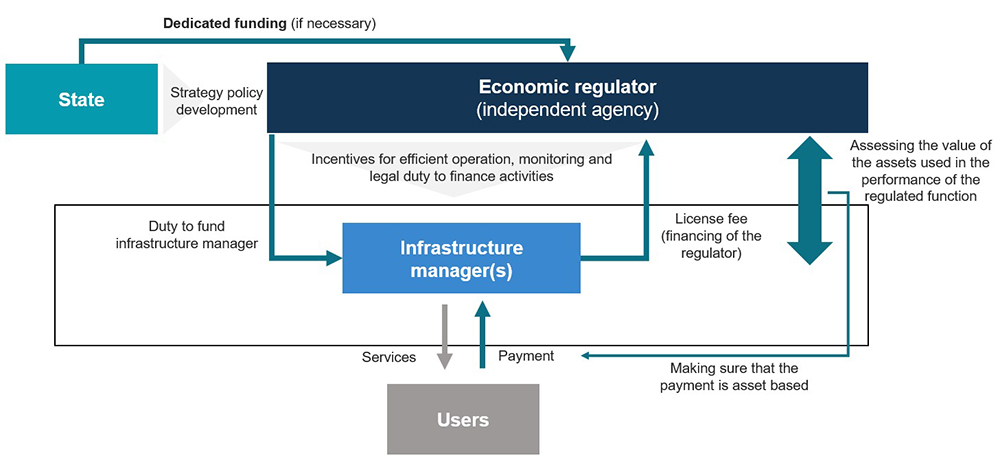

Apart from financing aspects, the critical question is what kind of entity would own and operate the CO2 pipeline network, where the decision again is between public and private ownership and operation. Due to their financing mechanisms, governments tend to have lower investment and operational costs but can lack operational efficiency because the operation of infrastructure assets is typically not a main part of their activities and expertise. The involvement of private actors in setups such as a public-private-partnership, on the other hand, can lack flexibility as long-term contracts between the government and private companies create lock-ins and rigidity. A middle ground option increasingly used in Europe for large infrastructures are Regulated Asset Base models (RABs). RABs allow a private or public infrastructure manager to operate under the supervision of an independent economic regulator. They combine the flexibility of government-owned infrastructure with the efficiency incentives of PPPs, allowing the infrastructure manager to operate in a monopolistic market while being kept in check by the regulator (see Figure 2).

Figure 2: Overview of organizational and financial models for shared network infrastructure

Variations of a RAB model have been utilized in Switzerland for the electricity grid and countries such as the UK which has indicated their intent to use the RAB model in their national CCS strategy. A similar RAB structure could be applied to the CO2 pipeline network in Switzerland, adapting existing regulated business models to fit the case of a CO2 network.

Outlook

Taking an outlook from Switzerland to Europe, one can conclude that countries increasingly build on best practices of network infrastructure management which lead to the increasing interest in developing and funding CO2 pipeline networks managed by RAB models. However, there are still several questions that need to be answered for this to be successful in Switzerland. For example, it is important to determine whether funding and organization should be at the federal or cantonal level, and what type of central operating entity would be appropriate for the infrastructure. Regardless, it appears that a centralized entity of some kind will be necessary to manage the infrastructure, coordinate between cantons, or connect to a larger integrated European network.

Authors

Martynas Bagdonas is a Project Manager at the sus.lab at ETH Zurich.

Oliver Akeret leads the decarbonization projects at sus.lab with a focus on carbon capture and storage (CCS) and carbon dioxide removal (CDR).

Reference

[1] CO2NET – Grobes Design und Kostenschätzung für ein CO2 Sammel-Netzwerk in der Schweiz: https://www.aramis.admin.ch/Texte/?ProjectID=47346